Strong Network of Branch Offices, More Opportunities for Financial Inclusion

The Branch Office of a small MFI is nothing like your local bank’s branch. There are no tellers, advisors, or bank staff to greet you when you walk in - that’s because rarely do clients walk in! Because Field Officers serve clients essentially "at their doorstep", or in their villages, the Branch Office is more of a home base and back-end processing center for staff. For Vaya specifically, ...

The Branch Office of a small MFI is nothing like your local bank’s branch. There are no tellers, advisors, or bank staff to greet you when you walk in - that’s because rarely do clients walk in! Because Field Officers serve clients essentially "at their doorstep", or in their villages, the Branch Office is more of a home base and back-end processing center for staff.

For Vaya specifically, a particular Branch Office may serve a host of villages within a 25 kilometer radius. As a result, for most clients, traveling to the local Branch Office is not something that is feasible, let alone on a biweekly basis.

While 25 kilometers may seem far, MFIs’ reach in rural India is in fact better than that of Indian banks - that is why many MFIs operate as Bank Correspondents. The only entity with a greater reach than MFIs across rural India is the Indian Post Office. According to their website, “India has the largest Postal Network in the world with over 1,54,882 Post Offices (as on 31.03.2014) of which 1,39,182 (89.86%) are in the rural areas.”

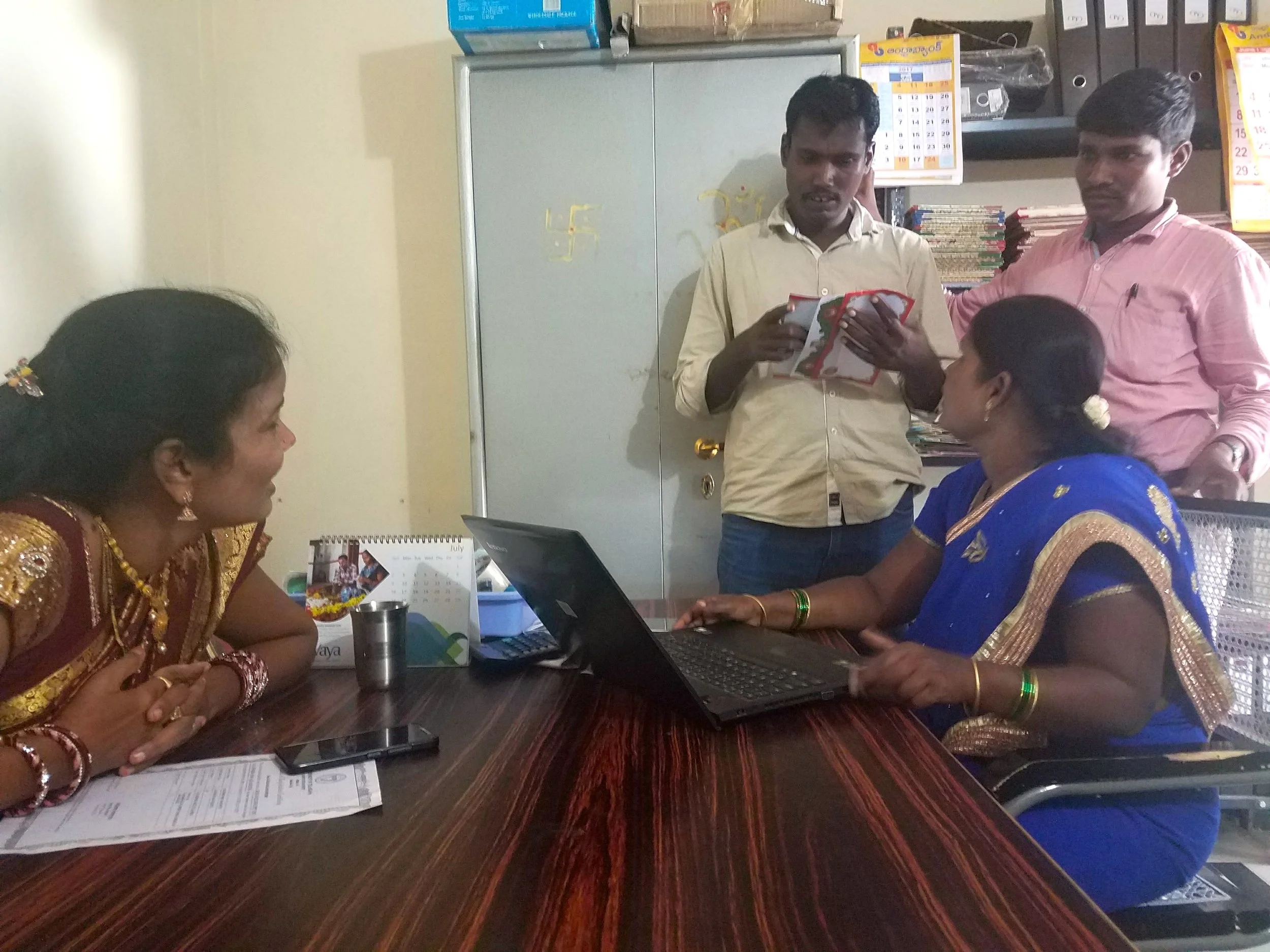

The local Vaya Branch Office in Narayankhed, Telangana. / June 21, 2017

After a morning of center meetings, where Field Officers meet with joint liability group members to collect their installments, Field Officers come back to their designated Branch Offices to recount the cash collected, carry out the denomination of the bills by value, and verify accounting records, before finally traveling to the nearest bank to deposit the day’s collections. Field Officers go back to the field in the afternoons to conduct further group meetings and reach out to new customers.

With the cash counted, accounted for, and safely stowed, the Field Officers chat for a bit. / June 21, 2017

While the transition to everything digital has already begun, installments are still collected in cash at the moment. However, following India’s recent demonetization, MFIs have begun to prioritize cashless payments, i.e. via bank transfers. Through demonetization, certain currency bills were taken out of circulation. Not only did cash become very hard to come by but those who transact primarily in cash, like the rural and urban poor, were the most adversely affected by the sudden lack of liquidity - many of them unable to make their installments. Therefore, by making bank transfers compulsory, MFIs would not only ensure that they receive their loan installments on time, and can continue to disburse new loans to other clients in need, but they can also help build a culture of banking amongst their clients, which may later facilitate delivery of other banking products beyond microcredit (savings, insurance, and more).

Two years ago, the Reserve Bank of India granted eight MFIs licenses to transition into small finance banks, precisely to facilitate the provision of further financial services to the urban poor. The Government of India is complementing the RBI's work through its own initiatives, focusing on getting all Indians to obtain a unique identifier (Aadhaar), a bank account (Jan Dhan), and mobile connectivity, also known as the JAM Trinity.

As I mentioned previously, Field Officers use tablets to record group member attendance, installment collection amounts, and other key details. However, because internet connectivity in rural India is not the most reliable, they also keep handwritten records to complement the digital ones. The application loaded on the Field Officers’ tablets allows for data entry now - independent of connectivity - and upload later, when a good enough connection can be established. Once the data is uploaded, it is readily available, in a matter of minutes, for analysis at the Head Office in Hyderabad.

As network connectivity improves, mobile penetration rises in rural areas, and banking know-how increases amongst rural dwellers, the possibilities for expanding financial services and providing more individuals with the funds they need to grow their businesses will only continue to grow. The MFI Branch Office, and its hardworking Field Officers, is just one of the main pillars in this growing network of support for hard-to-reach, aspiring entrepreneurs.

A Buffalo Today, A Thriving Business Tomorrow

My work at Vaya is well underway. In fact, today I reached the two-week mark! The work thus far has been fascinating, not only because of all I have learned about the evolution of microfinance - in India and around the world - but also because of the opportunity I have had to learn from industry leaders with many years of experience, to witness day-to-day operations, and to meet the very clients microfinance institutions (MFIs) like Vaya serve.

My work at Vaya is well underway. In fact, today I reached the two-week mark! The work thus far has been fascinating, not only because of all I have learned about the evolution of microfinance - in India and around the world - but also because of the opportunity I have had to learn from industry leaders with many years of experience, to witness day-to-day operations, and to meet the very clients microfinance institutions (MFIs) like Vaya serve.

My focus this summer will be on individual lending, and by the end of my nine weeks in Hyderabad I should be able to deliver:

- An overview of the existing market, products, competitors, and client needs

- An individual loan product design, associated process flow, and the required underwriting mechanism

- A weighted index to asses clients’ credit absorption, and

- A road map for the execution of the launch strategy

This week I had my first field visit, in the company of two colleagues, to see the group-lending mechanism in action. We traveled roughly two hours outside of Hyderabad, to a small town called Narayankhed. Narayankhed is the first village Vaya ever worked in. It is no coincidence that it is also where Vaya Chairperson and Tufts alumnus, Dr. Vikram Akula, opened his first microfinance branch when he headed SKS Microfinance (now known as Bharat Financial Inclusion Ltd., or BFIL).

My colleagues and I left Hyderabad before the crack of dawn in order to arrive in time to join one of the early morning center meetings. Vaya’s women borrowers come together biweekly at center meetings to confirm their commitment to the group, pay their installments, and plan for future loan disbursements. It was fascinating to see how organized the women were, ready to turn in their groups’ collective installments to the field officer, who expertly thumbed through the cash to verify the amount while using her work tablet to take attendance and record installment figures. At less than 15 minutes, the meeting was as efficient as could be, allowing the women to get to their morning work and home duties without much inconvenience.

After the meeting, I had the opportunity to meet with two of the women borrowers and hear from them about their experience with the lending process.

Vaya borrower Sutina graciously let me take a photo with her and her buffalo. / June 21, 2017.

Sutina (pictured above) recounted how she had saved INR 25,000 on her own (roughly USD 310) and then borrowed another INR 20,000 from Vaya to purchase a buffalo - the price was INR 60,000 (USD 930) but she was able to buy it for 50,000 (USD 775)! She milks about 6 liters from the buffalo per day and sells it to make a few hundred rupees. In a week’s time she has made a significant amount in profits, given that the buffalo grazes and the costs to feed it are minimal. Her confidence and pride in her work is remarkable. In addition to the income she receives through the buffalo, Sutina also mentioned that she often works as a day laborer - this means she goes out to look for work in agriculture or infrastructure projects in her town or other nearby towns. This is the most precarious type of work but can help rural families make ends meet.

I also met with Ghousia, who owns a kirana (small grocery) shop in Narayankhed. With the loan she was able to obtain through Vaya, she purchased a space big enough to set up her kirana and her husbands’ car repair shop - a modest establishment by Western standards but enough space to allow her husband to work from their village, rather than having to travel two hours to and from Hyderabad for work as he once did. Ghousia’s self-confidence shone through - so much so that she complained to me that she wanted me (Vaya) to offer larger ticket size loans so that she could expand her shop! I am working to help make that happen, more so now that I have Ghousia’s grievance cemented in my memory.

Vaya recently went from operating as a bank correspondent (BC), whereby it operated as an agent for a local bank called Yes Bank, to what the Reserve Bank of India denotes as a NBFC-MFI, or a non-banking financial company/MFI. Whereas as a BC Vaya is dependent on Yes Bank to be able to provide funds to its clients, now as a NBFC-MFI, it will be able to do so on its own - cutting loan application and processing times from as much as two months to a matter of days.

The individual lending model that I am exploring will also allow Vaya to serve the needs of mature clients that have gone though various loan cycles and obtained the largest ticket size loan it offers but who still need more capital to grow their businesses; it will also address the concerns of borrowers who - because of the larger ticket sizes and their growing financial literacy and confidence - no longer want to be liable for fellow borrowers through the joint liability group scheme.

For these reasons and many more, crafting an individual loan product is the next logical step in the company’s progression and clients’ growth.

During my trip, I also visited one of Vaya’s branch offices in Narayankhed, to get a closer look at all of the back-end work that most never see. Stay tuned for my next post on it!